What Is a Qualified Income Trust and When Is One Required?

Part of qualifying for long-term care Medicaid is meeting the strict financial criteria. For the institutionalized individual, this entails having income below the private pay rate of the Medicaid-approved facility where they reside. Certain states apply an additional income restriction if the applicant has income above a certain threshold. In these states, the applicant must establish a Qualified Income Trust (QIT).

Read More: 5 Things You Need to Know About QITs

What Is a QIT?

A QIT is an irrevocable, income-only trust with the Medicaid applicant acting as the grantor. Its purpose is to make income exceeding the state’s cap (typically $2,829 in 2024*) non-countable for Medicaid purposes. The funds from the trust are then disbursed each month for qualified care expenses as well as the individual’s Personal Needs Allowance, insurance premiums, and any applicable income shift to the community spouse under the Monthly Maintenance Needs Allowance rules.

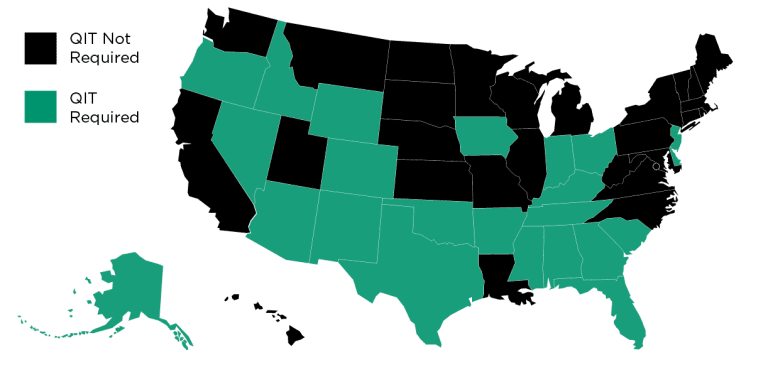

Which States Require a QIT?

Currently, the following 24 states utilize this extra income cap requirement: Alabama, Alaska, Arizona, Arkansas, Colorado, Delaware, Florida, Georgia, Idaho, Indiana, Iowa, Kentucky, Mississippi, Nevada, New Jersey, New Mexico, Ohio, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Texas, and Wyoming.

Additional Considerations When Establishing a QIT

When structuring a Qualified Income Trust, it’s vital to select the right trustee. After all, the trustee is responsible for managing the trust’s bank account and ensuring timely income payments and nursing home fees. Ideally, these payments are automated to minimize errors.

Another vital aspect of the trust is the payback provision, requiring any remaining funds upon the applicant’s death to reimburse the state Medicaid agency for expended benefits.

A potential hurdle in creating a QIT is the absence of a properly drafted power of attorney. If the applicant can’t establish the trust themselves, their agent or spouse may do so. However, if the power of attorney lacks authority to create a trust, or if there’s no spouse, court intervention might be necessary. Some states mandate specific language and proper execution in power of attorney documents for granting such powers.

Read More: How to Spend Down Assets for Medicaid

The Origin of the Qualified Income Trust

A Qualified Income Trust, also known as a Miller Trust, originated from the legal case Miller v. Ibarra and was later formalized by the Omnibus Reconciliation Act of 1992. Federal guidelines for the structure of the Miller Trust are detailed in 42 U.S.C. 1396p(d)(4)(b), though individual states have their own regulations, not to surpass federal restrictions.

If you’d like to learn more about Qualified Income Trusts and how to establish one for your client, contact our office today.

*Delaware is the only exception with an income cap of $2,358 in 2024.